App Store Growth Slows for Apple in 2022

IDFA and ATT: The Scapegoats of the Mobile Game Industry Slowdown?

2022 App Store Revenue: Little Change from 2021

On January 10th, 2023, Apple continued its tradition - announced that App Store developers have earned over $320 billion since 2008. This marks a $60 billion increase from the $260 billion Apple reported in 2021. This release suggests that the amount developers received in 2022 was little change from 2021.

In December 2020, Apple introduced a "Small Business Program" which lowered the company's revenue cut for app developers earning less than $1 million per year from 30% to 15%, effective January 1st, 2021. The program is expected to benefit the majority of App Store developers. While it's impossible to estimate the actual revenue from 2021 onward, given that Apple doesn't disclose the percentage of developers paying 30% vs. 15%, it's somewhere between $70.59 billion (assuming all revenue is subject to a 15% fee) and $85.71 billion (assuming all revenue is subject to a 30% fee). An estimated revenue using a 20/80 rule, with 20% of the revenue subject to a 15% fee and 80% of the revenue subject to a 30% fee, the estimated total would be $82.68 billion for 2021 and 2022.

Google's Play’s Revenue Dips in 2022 while Apple's App Store remains Flat

Google followed suit and dropped commissions to 15% from 30% on July 1st, 2021, with the same revenue threshold. Citing Google’s own estimates, Google said, "99% of developers that sell goods and services with Play would see a 50% reduction in fees, and that 97% of apps globally do not sell digital goods or pay any service fee."

IDFA and ATT: The Scapegoats of the Mobile Game Industry Slowdown?

The release of iOS 14.5, which includes the IDFA and ATT (App Tracking Transparency) changes, has raised concerns about its impact on the industry. While IDFA and ATT are often cited as contributing factors to the current slowdown by CEOs and marketers, it's worth noting that the industry was already showing signs of a potential slowdown prior to the pandemic. The pandemic not only prolonged the potential of a slowdown but also provided an once a lifetime opportunity for many companies to improve their operation, raise capital, and strengthen their balance sheets.

It's worth considering that there isn’t enough statistical evidence to support the argument of the changes in IDFA and ATT being the obvious suspects causing the slowdown in the mobile game industry. Though it came at a less-than-ideal time for sure, other factors like the economy, players returning to pre-pandemic behaviors, and pre-existing problems in the industry could also be playing a big role in the equation. It will likely take some time before we have a clear understanding of the actual impact of these changes.

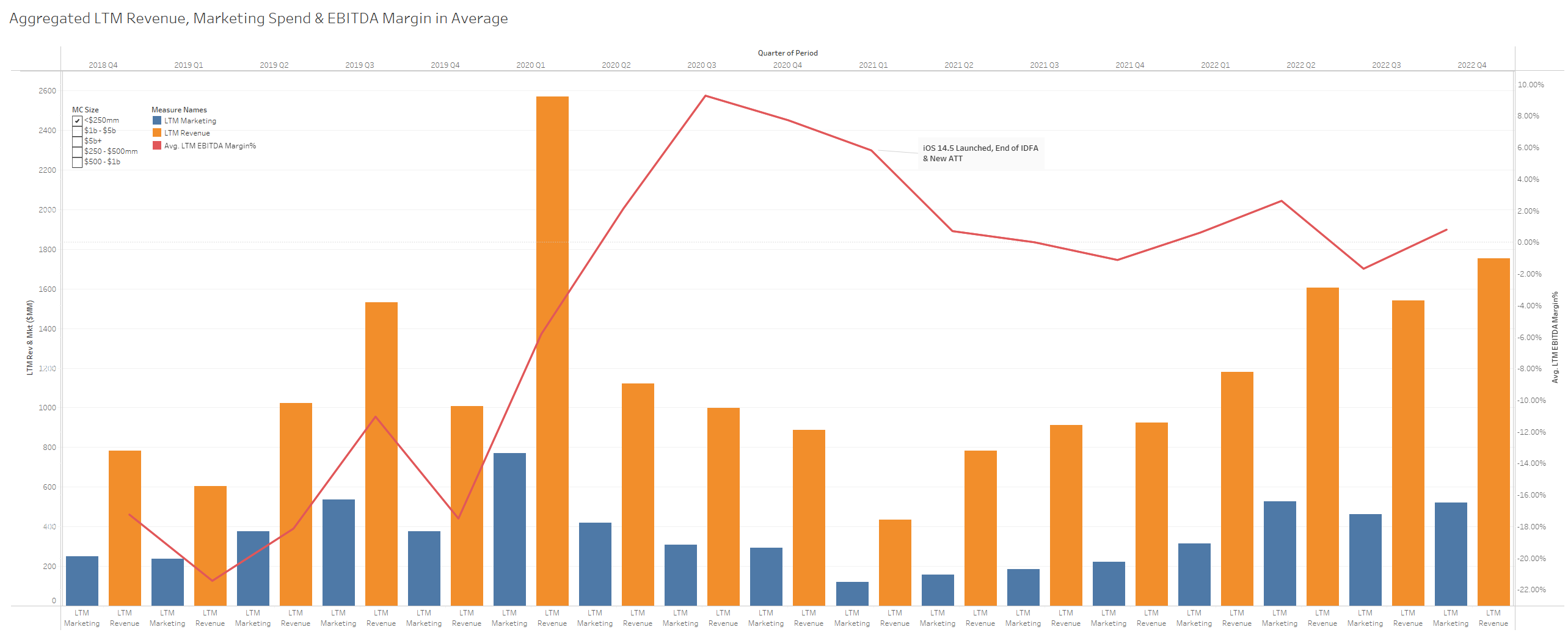

Annual EBITDA Margin by Market Cap Size

Companies with a market cap under $250 million saw an improvement in their EBITDA margin when compared to the pre-pandemic levels.

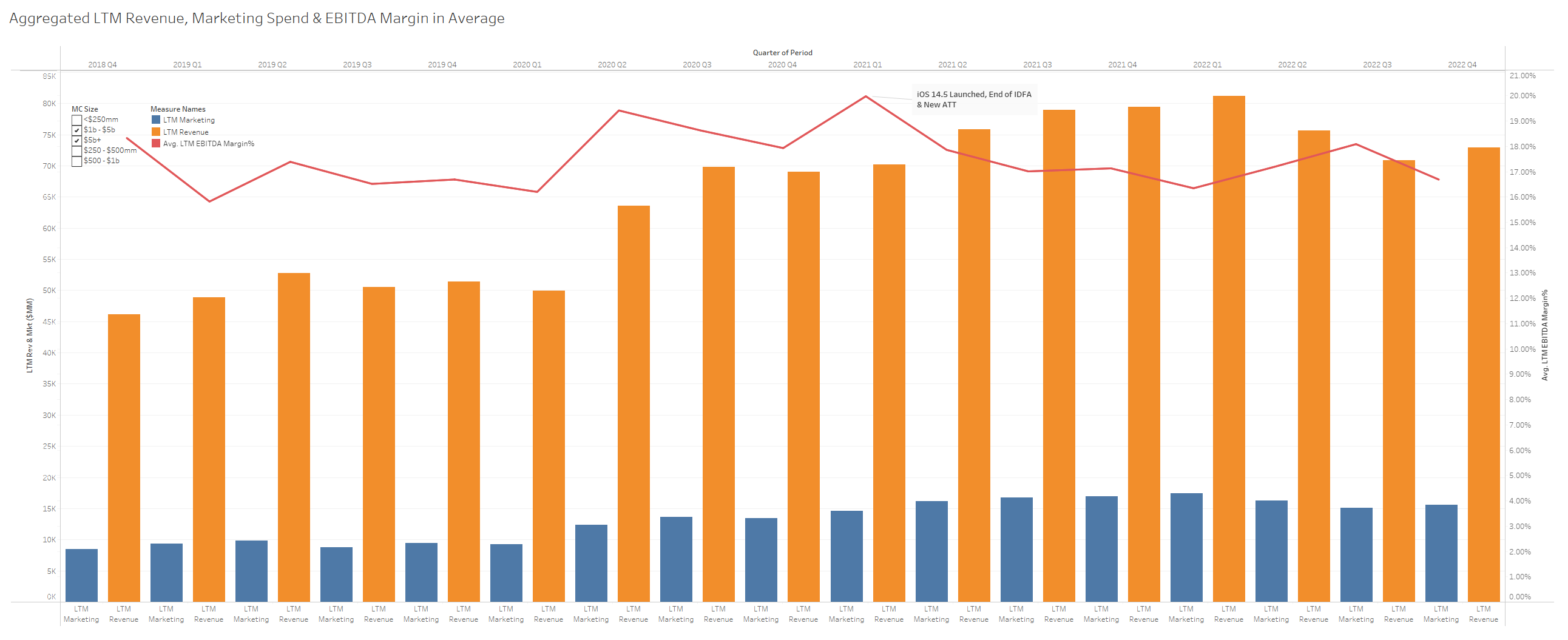

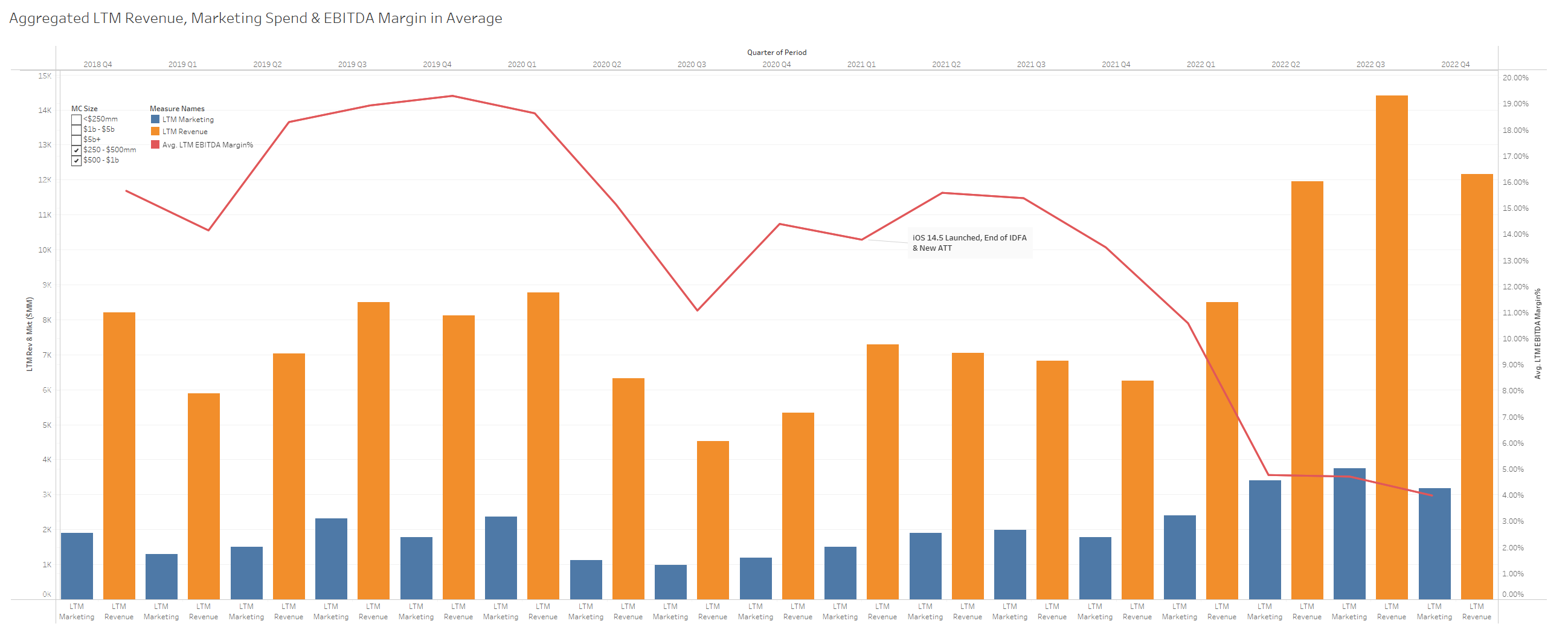

Quarterly LTM Revenue, Market Spend, & EBITDA Margin

Below is a summary of the financial performance of publicly traded mobile game companies over the past five years, presented quarterly. It includes information on their last twelve-month (LTM) revenue, marketing spending, and the average EBITDA margin for companies of different market capitalizations. Although it doesn't pinpoint the impact of iOS 14.5 on these companies, it can provide an understanding of the overall state of the mobile gaming industry and if there are any significant changes or trends.

Aggregated LTM Revenue, Marketing Spend & EBITDA Margin in Average - All Company Sizes

Aggregated LTM Revenue, Marketing Spend & EBITDA Margin in Average - $1+ Billion Market Cap

Aggregated LTM Revenue, Marketing Spend & EBITDA Margin in Average - $250 Million - $1 Billion Market Cap

Aggregated LTM Revenue, Marketing Spend & EBITDA Margin in Average - Under $250 Million

In the long run, I believe these changes could be a positive shift for the industry. Among industry professionals, there have been well-known issues, such as companies relying on an arbitrage model where they buy at a lower cost per install when they know/predict that they could generate a higher LTV over a period of time or extend their payback period to eliminate their competitors when they have stronger balance sheets. Clones and fast-food-like content have been flooding the market for some time because it was a lucrative strategy, until recently. Many C suites have focused more on user acquisition strategies and lifetime value modeling over game design and user experience. In less than a year, I’m observing a trend where companies are now more selective and cautious with their investments, carefully evaluating projects before committing resources. This is good news for mobile gamers.

A phrase I came across during my career that I found interesting for today’s world:

I’ve observed that many inexperienced founding teams who focus on creating great game experiences and know little about marketing have found great success. But I have rarely seen teams with a strong background in marketing but little knowledge of making great games achieve the same level of success.

To take a step back, the complexities of growing a game company through mobile marketing have never been easy, it wasn’t any easier before iOS 14.6.