Beyond the Bankruptcy: How Silicon Valley Bank's Collapse Affects the Ecosystem It Served

Included Line of Credit and Banking Help for Companies Impacted by SVB

Regardless of whether you work in the game/tech industry or not, you may have already heard about the recent news regarding Silicon Valley Bank. The unexpected collapse of SVB has the potential to trigger a chain reaction, depending on how much of their deposits businesses are able to recover and how quickly. Given the urgency of the situation, regulators are working diligently to devise a plan before Monday, March 13th. The clock is ticking.

Recovering 65 Cents on a Dollar - Worst-Case Scenario

In the worst-case scenario, businesses may be able to recover between 65% and 95% of their deposits, based on SVB's latest balance sheet report, even without FDIC or government intervention. However, the biggest challenge is the Monday deadline, as the need for speed and quality are often at odds with each other. The FDIC may require steeper discounts the faster they want to obtain liquidity. According to Bloomberg on Saturday, Venture and Capital management firms were offering to purchase the claims of SVB clients at discounts of between 60 and 75 cents on the dollar. This suggests that these firms are anticipating an outcome of between 80 and 95 cents on the dollar. The liquidity shortage for SVB is in the low single billion range, and these firms may step in to support the deposits once they have accumulated enough IOUs from SVB clients.

Small and Medium-Sized Businesses Are Disproportionately Affected

If you are a small to medium-sized business owner, it may be wise to reassess your cash flow and create a backup plan for the next six months while waiting for updates from the FDIC. Everything you were previously accustomed to could change dramatically as soon as next week.

The key to survival is to first focus on shoring up liquidity if all of your money is currently held up with SVB. If you have a Line of Credit, draw down as much as you need at least for the next three months. If not, here is a list of companies that offer Lines of Credit and/or banking assistance to companies affected by SVB (note: I have no affiliation with these firms, so please conduct your own research).

Second, reevaluate the feasibility of collecting your incoming receivables. Many affected companies will tighten their belts, potentially delaying or not paying their bills for non-essential expenses. If this sounds alarming, keep in mind that even Twitter, owned by the wealthiest man on earth, missed its payments on rent and AWS bills. It's a common business tactic to reprioritize resources to achieve specific objectives. While contractual obligations are important, the cost of enforcement and the time and probability of recovering your loss should also be considered.

Finally, prepare for a potential cash crunch. Review the terms of your Line of Credit with banks, vendors, marketing channels, etc. Some may reduce or cut off your LOC if the situation deteriorates, while others may even demand early repayment.

Uncertainty Remains Despite Full deposits Return

It's important to remain vigilant even if everyone receives 100% of their deposits back. Venture debt and financing will take time to recover from the recent events at SVB. SVB was unique for a reason - the products it offered were distinct in the banking industry, and not many banks will have the appetite or willingness to adopt them given the recent backlash.

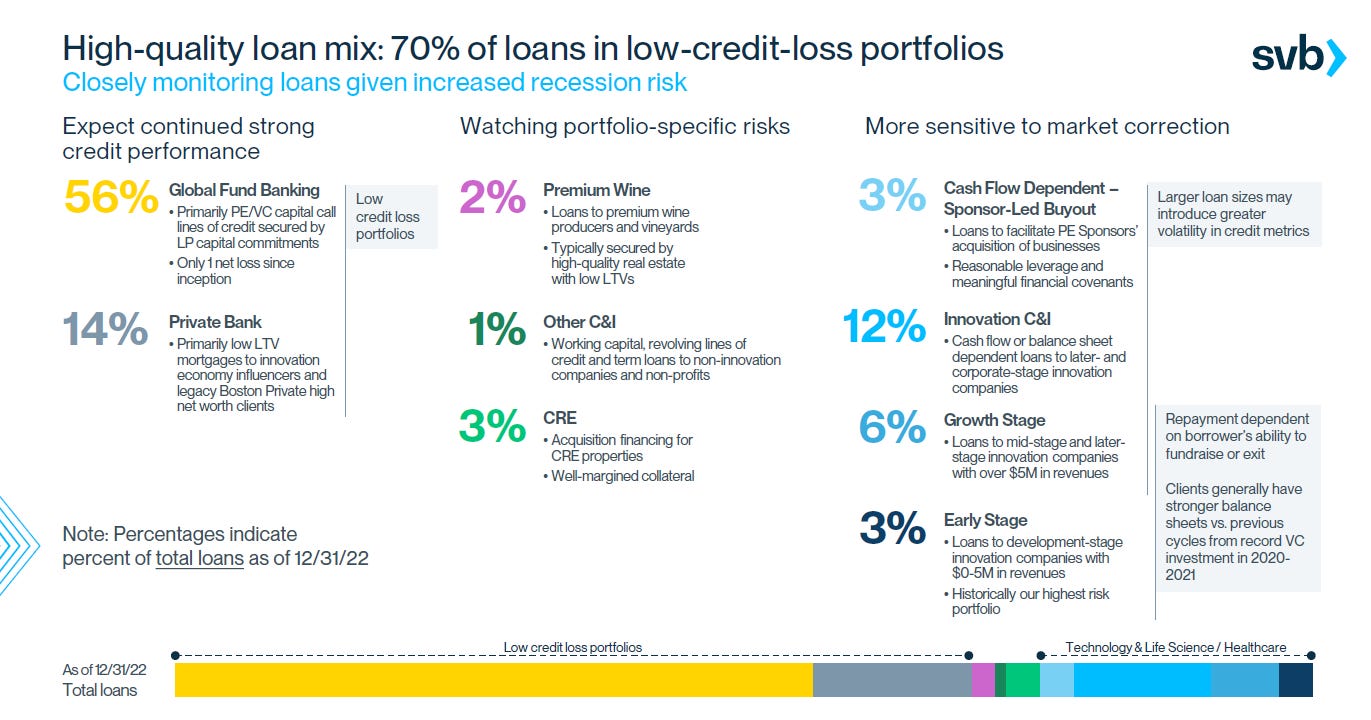

Many people have wondered why only 42 billion out of the 186 billion were withdrawn during the bank run. While 42 billion in one day is significant, it represents only about 25% of total deposits in an event like this. One reason why people did not withdraw their deposits is that they COULD NOT. SVB offered venture debt financing for private equity, venture capital companies, as well as mortgages for high-net-worth individuals. These clients were required to maintain a specific amount of deposits with the bank, among other restrictions, as part of their loan covenant. See below example for more details:

This is an incredibly challenging time for those who have been impacted, and I truly hope that you are able to recover from this setback soon. Please know that you are not alone in this, and that many are working to support those who have been affected. My thoughts are with you during this difficult time, and I wish you all the best as you navigate this situation.

Off Topic Question

I have a side question for myself. If there are any experts out there who have insights, please shed some light on the topic to satisfy my curiosity.

Did the bank simply engage in poor risk management by taking on too much duration risk, leading to mismatches in its assets and liabilities? The Federal Reserve has been telegraphing its intention to raise rates for weeks and even months in advance. Additionally, the Fed closely follows the 2-year Treasury yield and typically only halts rate hikes once the Fed Funds Rate exceeds the Consumer Price Index. Inflation is a persistent challenge, and it is obviously unwise to take significant duration risks in the early stages of the long-lasting hiking cycle. The asymmetric risk is like picking up pennies in front of a steamroller.